In recent years, corporate tax cuts have emerged as a hot-button issue in economic discussions, particularly following the controversial provisions of the 2017 Tax Cuts and Jobs Act (TCJA). This sweeping tax reform aimed to stimulate economic growth by significantly lowering corporate tax rates, provoking a vigorous debate about their long-term effects on corporate tax revenue and wage growth under tax cuts. Critics argue that the reduction in tax rates has led to substantial declines in the government’s corporate tax revenue, without yielding the expected increases in business investment or employee wages. Proponents, on the other hand, maintain that these tax cuts incentivize companies to expand and innovate, potentially driving a resurgence in employment and economic vitality. As Congress prepares for another tax policy debate, understanding the multifaceted impact of corporate tax cuts will be crucial for shaping future tax legislation.

In the evolving landscape of economic policy, discussions surrounding corporate tax reductions have gained renewed attention, particularly in light of the recent analysis of the 2017 Tax Cuts and Jobs Act (TCJA). This legislation aimed to revitalize the U.S. economy by lowering tax rates for corporations, sparking intense deliberation over its effectiveness in enhancing business investments and addressing corporate fiscal responsibilities. As the tax policy debate intensifies, many question the balance between fostering economic growth and maintaining adequate corporate tax revenue. Observers speculate that the implications of wage growth under tax reductions warrant careful examination, as the actual outcomes may diverge significantly from initial projections. With key provisions of the TCJA set to expire, the implications of corporate taxation strategies on future economic conditions remain a pivotal concern for policymakers and the electorate alike.

The Impact of the 2017 Tax Cuts and Jobs Act on Corporate Tax Rates

The 2017 Tax Cuts and Jobs Act (TCJA) marked a significant shift in the landscape of corporate taxation in the United States. By slashing the corporate tax rate from 35% to 21%, the TCJA aimed to stimulate economic growth and bolster investment among American businesses. However, while proponents claimed that such cuts would lead to increased capital investment and an expanded workforce, the reality has been more complex. Studies, including those conducted by economists like Gabriel Chodorow-Reich, reveal a modest impact on corporate behaviors and a substantial decrease in corporate tax revenue.

The reduction in corporate tax rates was intended to position the U.S. more competitively in a global economy where many countries had significantly lower rates. Despite this intention, the immediate aftermath saw a steep decline in tax revenue—by as much as 40% at the onset of the TCJA. This reduction raised questions about the long-term sustainability of such tax policies and whether they truly force corporations to invest in growth or simply allow for more substantial profit retention without significant reinvestment into the economy.

Debating Wage Growth Under Tax Cuts: Expectations vs. Reality

In the realm of wage growth, the impact of the TCJA has been widely debated. Initially, the Council of Economic Advisers anticipated significant wage increases, estimating a jump of $4,000 to $9,000 annually per full-time employee. However, subsequent analyses, including those conducted by Chodorow-Reich and his colleagues, suggest a far more conservative estimate of around $750 increase per worker in 2017 dollars. This disparity between expectation and reality raises crucial discussions on the effectiveness of tax policy in stimulating real wage growth and benefits for the average worker.

Critics point out that by prioritizing corporate tax cuts, the TCJA may have diverted attention and resources away from policies aimed at directly enhancing wages for workers. While higher profits and increased capital investments are beneficial to corporate growth, translating these gains into wage increases for employees remains essential for a balanced economy. Such nexus is crucial during tax policy debates as lawmakers grapple with finding a middle ground that balances benefits for corporations and tangible benefits for workers.

Corporate Investments and the Role of Expensing Provisions

One critical aspect highlighted by the analysis of the TCJA is the role of expensing provisions in driving corporate investments. These provisions allowed businesses to write off the full cost of new capital investments immediately, which in contrast to statutory rate reductions, targeted growth more efficiently. The evidence gathered post-TCJA indicates that capital investments indeed surged by approximately 11%, suggesting that well-structured tax incentives can stimulate growth more effectively than broad rate cuts.

Chodorow-Reich argues that policymakers should consider reinstating these expensing provisions alongside moderate increases in corporate tax rates to foster an environment where business investment translates into higher wage growth. Such a strategy could create a beneficial cycle, where expanded investments necessitate hiring more workers, thereby increasing demand for labor and ultimately leading to wage increases across various sectors.

Tax Policy Debate: Analyzing Post-TCJA Outcomes

As the expiration of key provisions draws closer, the tax policy debate intensifies. The TCJA has become a partisan battleground, with Democrats advocating for increased corporate tax rates to fund social programs while Republicans push for a continuation or even further reductions of corporate tax cuts to drive growth. The contrasting narratives surrounding corporate tax cuts often overlook nuanced evidence from studies that show while there was some increase in business investments, the overarching fiscal implications may not favor the anticipated corporate tax revenue generation.

This ongoing debate underscores the need for more comprehensive evaluations of the TCJA’s impacts, particularly regarding its long-term implications for corporate tax revenue and economic stability. Stakeholders, ranging from economists to policymakers, must weigh the benefits of corporate tax cuts against the backdrop of declining revenues and seek innovative approaches to tax reform that encourage corporate growth while also ensuring adequate funding for public services.

Future of Corporate Taxation: Lessons from the TCJA

Looking ahead, the lessons learned from the TCJA could greatly inform future tax legislation. Although it offered relief to corporations, the dramatic decline in tax revenue raises important questions about how sustainably such tax cuts can function in the broader economic ecosystem. Economists like Chodorow-Reich emphasize the importance of evaluating both short- and long-term outcomes of such tax policies to devise a balanced taxation system that promotes equitable growth.

The landscape of corporate taxation is likely to continue evolving, especially as politicians assess the implications of expiring provisions in 2025. A thoughtful approach to corporate taxation—one that includes both consideration of statutory rates and targeted investments through expensing provisions—can facilitate business growth while securing necessary revenue streams for the government.

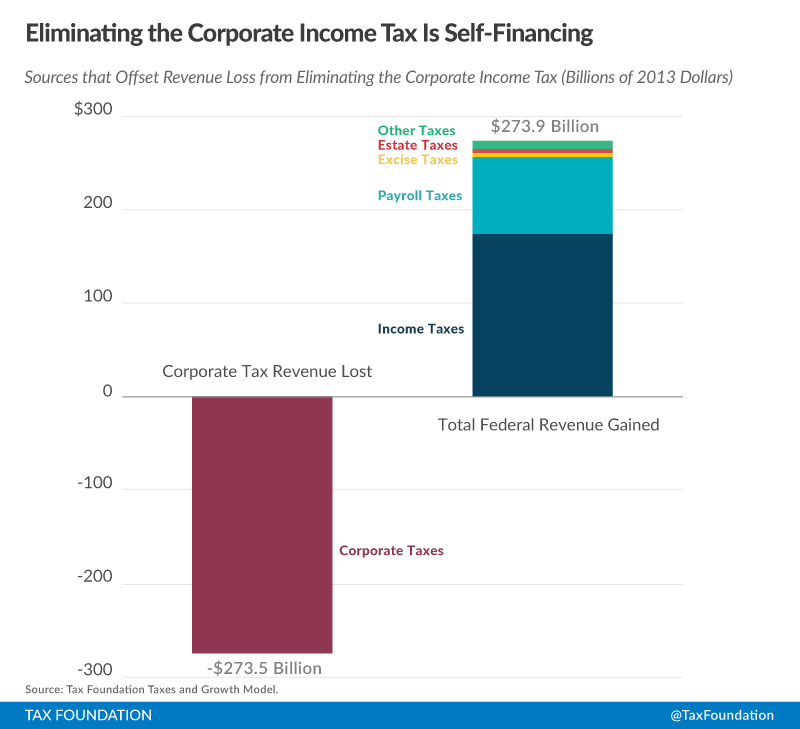

Effect of Corporate Tax Cuts on Government Revenue

The substantial cuts in corporate tax rates under the TCJA resulted in an immediate and notable decline in federal corporate tax revenue, which decreased by approximately 40% upon implementation. This dramatic shift has prompted analysts to scrutinize the long-term viability of maintaining such low corporate tax rates while still adequately funding government functions. Understanding the intricate relationship between tax cuts, business profits, and corporate tax revenue remains vital for ongoing fiscal planning.

While corporate profits have surged post-TCJA, often exceeding forecasts, the initial drop in tax revenue poses challenging questions for fiscal policymakers. Recent findings indicate that corporate tax revenue began to recover around 2020, suggesting that external factors, like economic adjustments amid the pandemic, could also influence revenue flows. Future discussions may benefit from examining how corporate tax policy can be adjusted to recapture lost revenue while still promoting investment and growth.

Evaluating Economic Competitiveness Post-TCJA

The TCJA aimed to make the U.S. more competitive by lowering corporate tax rates significantly, yet whether it achieved this goal remains a point of contention. With shifting global landscapes and comparative tax rates, the essential question becomes whether these cuts have resulted in tangible returns, such as enhanced competitiveness in attracting international businesses and investment. Economists argue that while initial corporate investment may have risen, sustained growth and global competitiveness depend much more on an array of factors, including regulatory environments and workforce quality.

Furthermore, the evolving landscape, particularly as other nations adjust their corporate tax rates, could necessitate further revisions to U.S. policy. A strategic balance must be struck to ensure that competitive tax rates do not come at the expense of essential social investments needed within the U.S. economy. Evaluations of the TCJA’s effectiveness indeed must look beyond mere rate cuts to understand the broader implications of these policies over time.

Understanding the Broader Economic Impacts of Tax Cuts

The comprehensive evaluation of the TCJA offers insights that transcend individual corporate tax policies, broadening the understanding of how tax cuts influence various aspects of the economy. While proponents argue that tax cuts foster economic growth by increasing business investments, studies reveal that the actual return on investment for workers is often less pronounced than expected. Thus, recognizing the broader economic ramifications of tax cuts is crucial in shaping effective fiscal policies.

As discussions around the implications of tax policies continue, understanding corporate tax cuts’ impact on revenue generation, wage growth, and overall economic health is essential. The TCJA serves as an important case study for guiding future tax reforms and ensuring that they are designed to foster inclusive economic growth and stability.

The Role of Political Narratives in Shaping Tax Policy

In the politically charged atmosphere surrounding corporate tax policy, narratives often shape public perception and legislative priorities. The TCJA’s considerable tax cuts sparked varied reactions from political extremes, with Republicans championing tax liberalization as a means to promote economic activity, while Democrats have rallied for raising corporate tax rates to address budget shortfalls and bolster social programs. This ongoing dichotomy reflects how tax policy debates are framed by broader economic ideologies and objectives.

To move past entrenched partisan narratives, it is crucial to base discussions on empirical evidence regarding the effects of corporate tax cuts. A data-driven approach can help move the conversation toward identifying balanced tax solutions that can promote healthy corporate growth while ensuring that the needs of the wider economy and society are not overlooked.

Frequently Asked Questions

What are the impacts of corporate tax cuts from the 2017 Tax Cuts and Jobs Act?

The corporate tax cuts from the 2017 Tax Cuts and Jobs Act significantly reduced the corporate tax rate from 35% to 21%. According to analyses, this led to modest increases in wages and capital investments but did not offset the substantial drop in corporate tax revenue, which fell by approximately 40% immediately after implementation before beginning to recover in 2020.

How did the 2017 Tax Cuts and Jobs Act affect corporate tax revenue?

The 2017 Tax Cuts and Jobs Act caused an immediate 40% drop in federal corporate tax revenue. However, by 2020, corporate tax revenue started to recover and even surged above expectations as business profits increased significantly, partly due to economic adjustments post-pandemic.

What was the tax policy debate surrounding corporate tax cuts in 2025?

The tax policy debate surrounding corporate tax cuts in 2025 centers on whether to renew the significant reductions enacted by the 2017 Tax Cuts and Jobs Act, set to expire, or to raise corporate tax rates as proposed by some lawmakers to fund various initiatives. This conflict reflects broader partisan disagreements on the effectiveness of corporate tax cuts and their impact on economic growth.

Did corporate tax cuts lead to wage growth as predicted?

Predictions prior to the enactment of the 2017 Tax Cuts and Jobs Act suggested that corporate tax cuts would lead to wage increases of $4,000 to $9,000 annually per full-time employee. However, studies following the law’s implementation indicated more modest wage growth of approximately $750 annually, challenging the initial optimistic forecasts.

What is the effect of corporate tax cuts on investment in the economy?

The 2017 Tax Cuts and Jobs Act was found to increase capital investments by about 11%. While traditional corporate tax rate cuts benefit existing capital and new investments, specific expensing provisions were identified as more effective at driving growth in business investments, reflecting a targeted approach to stimulating economic activity.

How do corporate tax cuts affect long-term economic growth?

The long-term economic growth effects of corporate tax cuts, such as those from the 2017 Tax Cuts and Jobs Act, can be complex. While proponents argue that lower rates encourage investment and job creation, recent analysis shows that the corresponding increases in wages and overall tax revenue, especially after the immediate drop, are less straightforward than initially claimed.

What lessons can be drawn from the 2017 Tax Cuts and Jobs Act regarding corporate tax policy?

The analysis of the 2017 Tax Cuts and Jobs Act underscores that corporate tax policy significantly influences business behavior, investment levels, and ultimately economic performance. It suggests that multi-faceted approaches, such as combining rate adjustments with targeted expensing incentives, may yield better outcomes for both growth and revenue.

Will corporate tax cuts remain a key issue in future tax policy debates?

Given the expiration of important provisions of the 2017 Tax Cuts and Jobs Act by 2025, corporate tax cuts will likely remain a central issue in ongoing tax policy debates. The discussion will revolve around their effectiveness in fostering economic growth versus the need for increased revenue to support federal initiatives.

| Key Points |

|---|

| 2017 Tax Cuts and Jobs Act (TCJA) cut corporate tax rate from 35% to 21%. This change was a response to international competition. |

| The TCJA is a significant point of debate as important provisions are set to expire by end of 2025. |

| The law resulted in modest increases in wages and business investments, but tax revenue dropped significantly. |

| Economic analyses suggest that some expired provisions were more effective in driving investment than rate cuts. |

| Corporate tax revenue fell initially but began to recover in 2020 amidst higher than expected business profits. |

| Future tax policy discussions are likely to explore raising statutory rates in conjunction with restoring expensing provisions. |

Summary

Corporate Tax Cuts have been a contentious issue since the enactment of the TCJA in 2017. As key provisions approach expiration, the debate intensifies among lawmakers regarding the balance between corporate tax cuts and the federal tax revenue that is needed to fund essential services. Research indicates that while corporate tax cuts may stimulate some growth in wages and investments, they have significantly reduced tax revenue which is crucial for the economy. The ongoing discussions will likely focus on how to make corporate tax policies more effective, balancing investment promotion with the need for adequate government revenue.

Leave a Reply